Choosing the right medical insurance for home-based care requires a clear view of needs, policy language, and provider networks. Start by listing the types of at-home services you or a loved one will need and how frequently they will be required. Knowing whether care is short-term after an event or ongoing chronic support will shape which plans are appropriate. Use this foundation to evaluate coverage options and anticipate out-of-pocket costs.

Review your current plan documents and note any exclusions related to in-home services. Gather recent medical records or care assessments to inform conversations with insurers and providers. Staying organized early reduces surprises when you need services most.

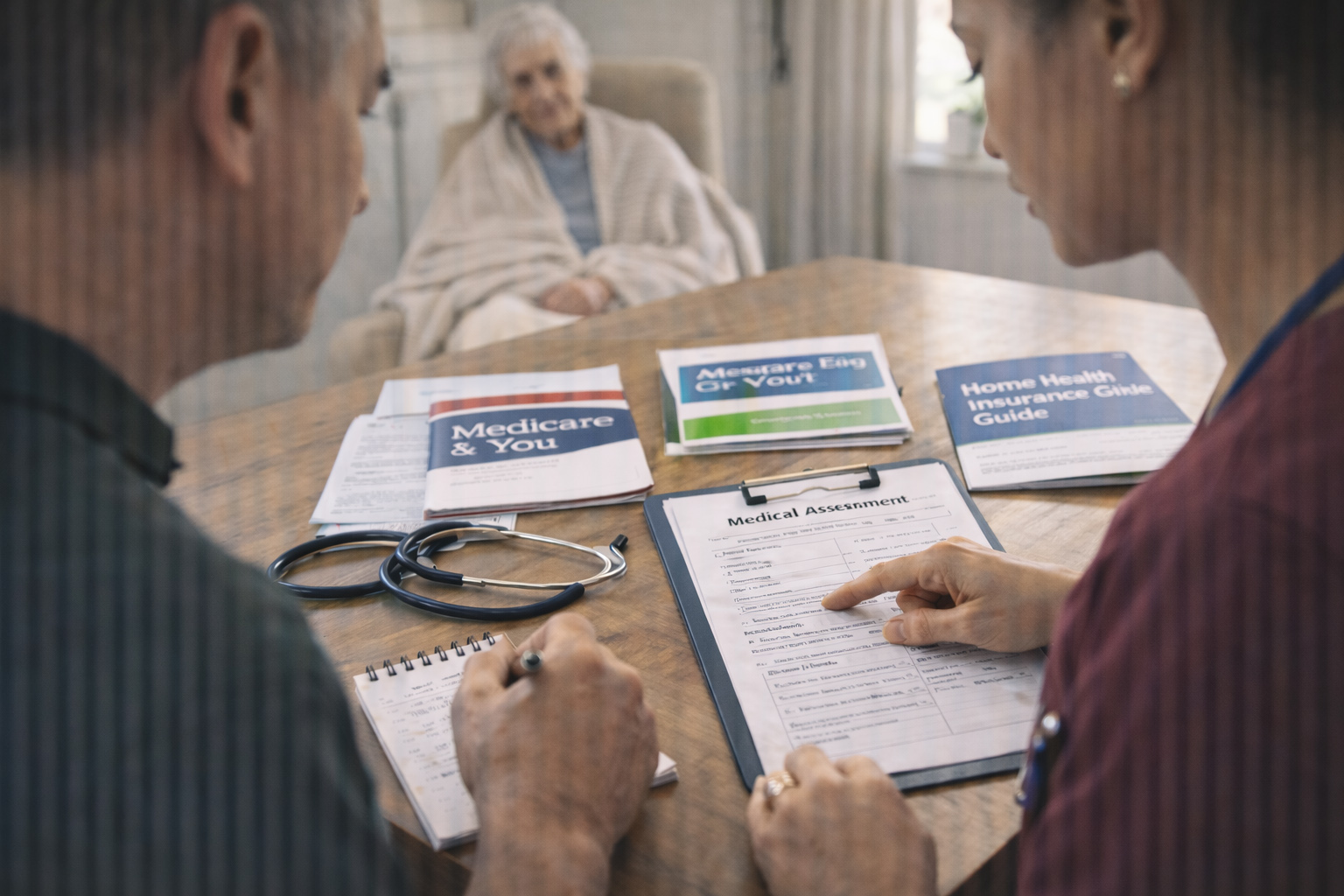

Understanding Coverage Basics

Medical insurance for home health typically covers services that would otherwise be provided in a clinical setting when they are medically necessary. Coverage can include skilled nursing, physical therapy, occupational therapy, and some medical equipment, but benefits differ widely by policy. Pay attention to definitions of “home health” versus custodial or personal care, since the latter is often excluded. Also check prior authorization requirements and any caps on visits or dollar limits.

Make a list of frequently used benefits and verify them with your insurer in writing. This creates a clear record if disputes arise later.

Assessing Personal Care Needs Versus Policy Limits

Match the assessed care needs to what a policy covers by comparing frequency, provider type, and duration. An occupational therapist twice weekly differs substantially from daily personal assistance, and policies treat those services differently. Consider the training requirements for covered providers, as some plans require licensed clinicians rather than aides. Factor in assistive devices and home modifications which may be partially covered under durable medical equipment or separate rider options.

Prioritize services that directly impact safety and independence when negotiating coverage or selecting providers. Flexibility in scheduling and provider choice can be just as important as headline benefit limits.

Tips for Choosing and Using Benefits

When evaluating plans, request sample benefit explanations for hypothetical scenarios that mirror your likely needs. Ask about in-network home health agencies and whether out-of-network providers can be approved. Keep detailed notes of all communications, claim numbers, and provider reports to streamline approvals. Consider supplemental policies or riders that cover gaps like long-term custodial care if needed.

Schedule annual reviews of your coverage as needs evolve and as insurers update plan terms. Small adjustments ahead of time often prevent major disruptions later.

Navigating Claims, Appeals, and Coordination

Submit complete documentation with initial claims, including physician orders and care plans that establish medical necessity. If a claim is denied, use the insurer’s formal appeal process and include additional supporting evidence, like progress notes and functional assessments. Coordinate between primary clinicians, home health agencies, and case managers to present a unified case for coverage.

Engage a patient advocate or ombudsman for complex denials to improve outcomes. Persistence and clear records often lead to successful appeals.

Conclusion

Carefully align assessed home health needs with policy definitions and limits. Keep thorough documentation and verify benefits in writing to avoid surprises. Regularly review and adjust coverage as needs change.